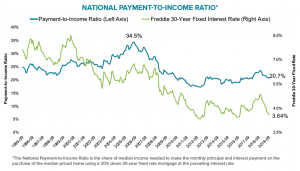

As of the end of September–with 30-year rates at 3.64%–20.7% of the national median income was required to make the monthly principal and interest (P&I) payments on the average-priced home. That's according to Black Knight's newly released Mortgage Monitor Report.

This is the second lowest payment-to-income ratio in 20 months (behind only August 2019), and 4.5% below the long-term (1995-2003) average. Affordability hit a 32-month high in early September–albeit briefly–when interest rates dipped below 3.5% for a single week and brought the payment-to-income ratio down to 20.3%.

The $1,122 in monthly P&I required to purchase the average home is down 10% from November–when interest rates peaked near 5%–despite home prices rising more than 4% from that point. Affordability hit a nine-year low back in November, spurring a noticeable and extended slowdown in home price growth. The decline in rates since then has been enough to boost buying power by $46K (+16%) while keeping monthly P&I payments the same.

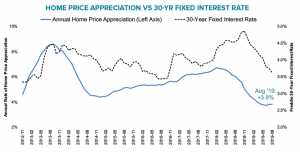

Despite improving affordability, annual home price growth held flat at 3.8% in August after rising for the first time in 17 months in July. Keep in mind that June’s annual home price growth rate of 3.7% was the lowest in nearly seven years before reversing course and edging up slightly in July. The fact that the strongest gains in–and strongest levels of–affordability were in August and early September could bode well for September/October housing numbers, though.

Despite improving affordability, annual home price growth held flat at 3.8% in August after rising for the first time in 17 months in July. Keep in mind that June’s annual home price growth rate of 3.7% was the lowest in nearly seven years before reversing course and edging up slightly in July. The fact that the strongest gains in–and strongest levels of–affordability were in August and early September could bode well for September/October housing numbers, though.

"It remains to be seen if this is merely a lull in what could be a reheating housing market, or a sign that low interest rates and stronger affordability may not be enough to muster another meaningful rise in home price growth across the U.S.," says Black Knight Data & Analytics President Ben Graboske. "We’ll be keeping a close eye on the numbers coming out of the Black Knight Home Price Index over the coming months.”

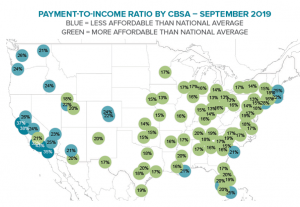

While affordability has improved across much of the country, pockets of tight affordability remain, most notably on the West Coast.

In fact, California now accounts for seven of the 10 least affordable markets in the nation, despite interest rates at or near multi-year lows. In L.A., for example, purchasing the average-priced home requires nearly 43% of the median household income–more than twice the national average.

While much better than the nearly 71% required in 2006–or even the 48% back in November--that still makes Los Angeles the nation’s least affordable housing market. The Midwest continues to be the most affordable.

See Black Knight’s August 2019 Mortgage Monitor Report for additional details.