!--more-->

Thankfully, we have companies like Fannie Mae and Freddie Mac who have mandates to keep housing affordable for Americans.

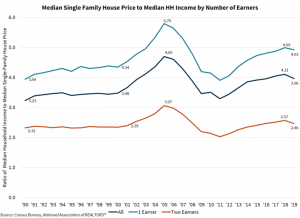

In response to this disparity between the rise in wages versus home prices, Doug Duncan, Senior Vice President and Chief Economist at Fannie Mae said “the rise of women in the workforce has changed the dynamics of house prices to reflect an expectation of two incomes. If you look at median house price in a market relative to median income of a two- person household, it’s at long term normal levels. If you have only one income, that is where the affordability problem is.”

So, it’s not so gloomy, it is societal trends running their course.

The accelerated increase in house pricing is being driven by several factors:

- The cost of the big three components – land, labor and lumber – have all increased. Lumber cost is at an all-time high. With lower levels of immigration, labor costs have increased and, with strict zoning regulations, especially in urban settings, land has been limited and the price driven up.

- Low interest rates, which are expected to remain at existing levels though this year, have made borrowing more affordable. That same monthly payment can now buy more house, driving up buyers’ bids.

- The supply/demand imbalance, which is perhaps the biggest factor. On January 22nd, the National Association of Realtors announced that unsold housing inventory sits at an all-time low of 1.9 months based on the current sales rate. That's down from 3 months a year ago. Demand, driven by low interest rates and societal shifts due to Covid-19, has outpaced supply.

Why the shortage of houses for sale?

Many people, especially older people driven by COVID-19 concerns, who own homes don’t think now is a good time to sell. In December, the Fannie Mae Home Purchase Sentiment Index® (HPSI) declined for the second consecutive month and fell to its lowest level since May 2020 as consumers adjusted to the worsening COVID-19 conditions of the first few weeks of December.

"Both the ‘Good Time to Sell’ and ‘Good Time to Buy’ components fell significantly, with respondents overwhelmingly noting the unfavourability of economic conditions,” Duncan said. “In particular, the sell-side component fell for the first time since April and by 18 points, reversing most of the increases of the past three months and implying to us that, at least temporarily, potential home sellers might wait to list their homes. If so, this could have the effect of perpetuating already-tight inventory levels and supporting additional (albeit lesser) home price growth, which could contribute to a further moderating of home sales.” When supply falls more sharply than demand, prices increase.

Supply is Expected to Increase Going Forward

The U.S. Commerce Department announced that housing starts jumped 21.4% on a year-over-year basis and building permits soared 9.2%, the highest level in 13 years. “The good news about the house rise is that markets are performing the way you would expect. When prices go up and profits go up that is a signal for others to enter production and increase supply, and that’s certainly happening,” Duncan said. However, it might take a while for the supply to catch up with demand. Experts say that homebuilders and construction companies will have to continue these increased efforts though 2022 to meet demand levels.

It’s Not Just About Building More Houses

More people may be putting their houses on the market as well. As the HPSI indicates, there is pent up demand on the sell side.

Also, the MBA estimates that 5.54% of mortgage loans are in forbearance. When forbearance ends, some homeowners will be faced with a tough choice, either sell or get foreclosed upon. Unless they bought very recently, chances are they have built up enough equity to make selling the best option. This too will add to inventory levels.

The impact of the end of forbearance on the housing market is a matter of debate, but Fannie Mae sees the impact as one reason it is forecasting housing appreciation in 2021 to be 4.5% rather than the 10% of 2020. (Note: the historical norm for annual price increase is 3.75%)

Millennials were already starting to move from urban to suburban areas. During the financial crisis Millennials were looking for jobs and the places they were available was in the urban centers. This meant many lived in apartments. Now that they have children that are reaching school age they are moving out to areas with more land, more sports, good schools and other amenities.

They are moving from urban areas to the suburbs. When COVID-19 hit, the plans these people had for the next three years accelerated. The recent housing starts data support this, showing single family housing starts rose 12% while multi-family fell 13.6%.

How sustainable this movement is remains to be seen. If this is just an acceleration of buying that would have happened anyway, it implies that the supply/demand balance would move toward more supply, less demand a few years out.

There are a lot of factors at play when it comes accessing the cost of housing. It seems that the house prices will continue to rise in the short term and have the potential to grow at a slower pace, or even decline slightly, a few years out. With that said, if you have to borrow to buy a house, now is a good time to buy. You might just have to be more patient or more aggressive than you would have been otherwise given the competition.